TL;DR

- Web3 companies face systematic challenges in getting traditional banking services due to legacy compliance models, correspondent banking pressure, and regulatory uncertainty.

- A true crypto-friendly business account is a regulated financial platform made intentionally for companies that use both digital assets and fiat.

- Providers of crypto business accounts differ significantly by licensing structure.

- For most Web3 businesses, combining on-chain treasury with on demand conversions and payouts is the most scalable approach.

For any company operating with digital assets, accessing basic financial services like payments, corporate cards, expense management, etc., for your business is hard. It's a structural problem as legacy compliance frameworks inside traditional banks were not built for blockchain-native business models. A possible alternative? A crypto-friendly business bank account.

What Is a Crypto-Friendly Bank Account for Businesses?

A crypto-friendly business account is typically a regulated financial platform purpose-built for companies that operate with digital assets alongside fiat. The regulatory status and oversight behind these platforms can differ significantly by provider and jurisdiction. Standard business bank accounts are designed for fiat-only operations and typically reject businesses with blockchain-sourced funds or on-chain treasury arrangements. A crypto-friendly platform accepts these as operational realities.

How it differs from a traditional business bank account

A traditional business bank account typically holds fiat, receives fiat, sends fiat, and evaluates clients through legacy risk criteria. A crypto-friendly platform connects to digital asset treasuries, processes digital assets payments i.e., cryptocurrencies or stablecoins, and supports cross-border transfers on modern payment rails, all from one account.

Why Crypto Companies Struggle with Banking

Crypto and web3 organizations often have trouble with accessing banking services like opening business bank accounts - why is it so?

The de-banking problem and why traditional banks say no

Traditional banks and business account providers are built around assumptions that do not match how many Web3 businesses operate. The friction is structural rather than personal, and it falls into three areas:

1. Compliance frameworks not built for on-chain activity

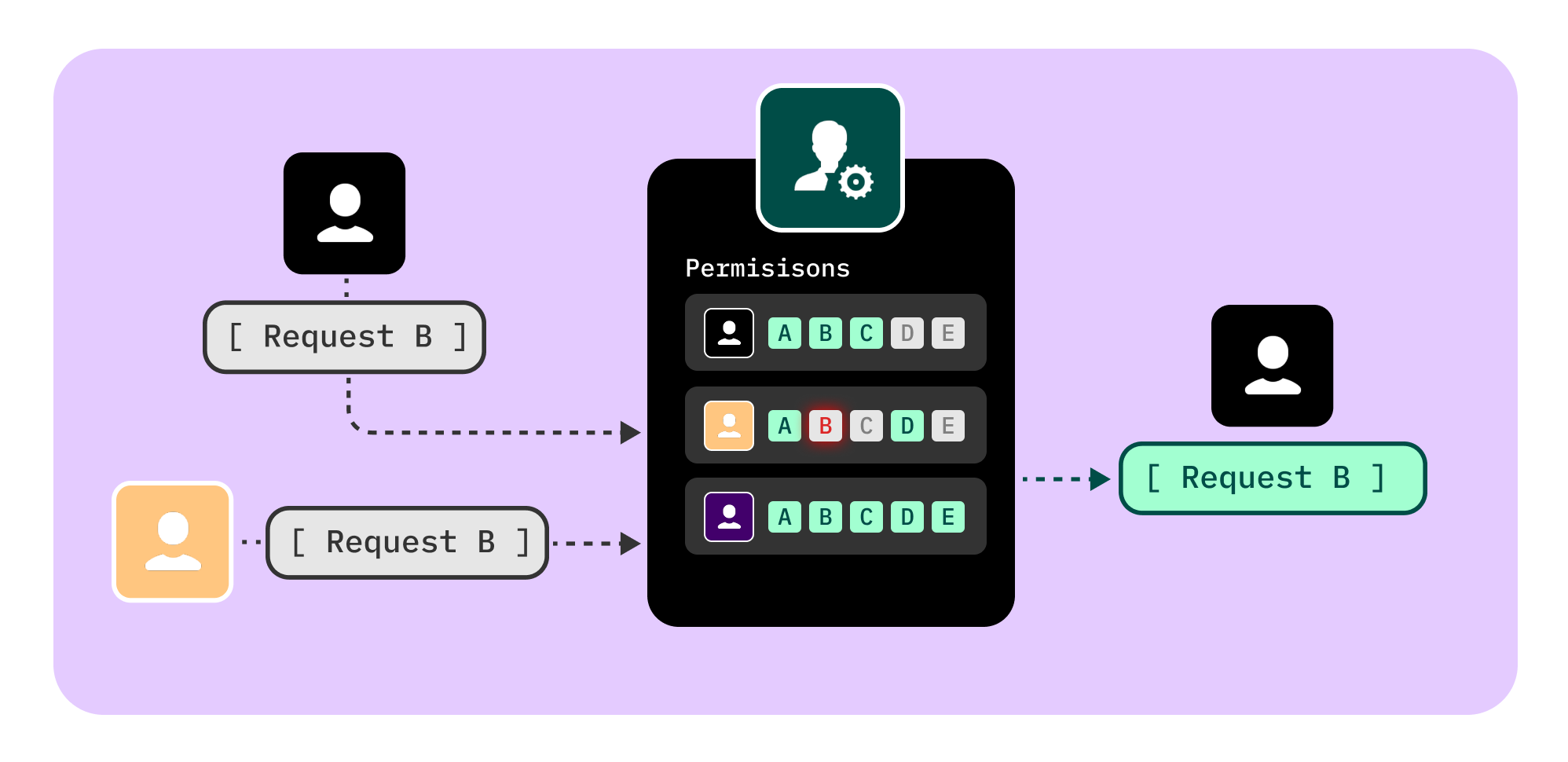

Banks must meet strict Know Your Customer (KYC), Anti-Money Laundering (AML), sanctions screening, and source-of-funds requirements. Web3 businesses may receive funds from wallets rather than bank accounts, hold treasury assets on-chain, and transact with on-chain counterparties across multiple jurisdictions. Those characteristics create compliance complexity that most banks' frameworks cannot map to their standard risk assessment process. Most institutions route crypto-exposed businesses into extended Know Your Business (KYB) and enhanced due diligence cycles that many prefer to avoid entirely by declining at onboarding, often without a specific reason.

2. Corporate structure and ownership that doesn't map to standard KYB

Standard KYB procedures typically require a bank to identify who owns and controls the business. Many Web3 companies operate with multi-entity structures across jurisdictions, or with governance and treasury arrangements such as decentralised autonomous organization (DAO) multi-sig setups that do not resemble a standard operating company. Ownership and accountability that are difficult to map to identifiable individuals within the bank's existing documentation framework result in the application being treated as higher risk or declined rather than processed through a custom compliance path.

3. Correspondent banking pressure

Even when a bank is willing to serve a crypto business, the bank may be structurally unable to. Most small and mid-sized banks access global payment networks through larger correspondent banks, and those correspondents often maintain blanket policies against transactions touching digital assets. A regional bank that serves a crypto client risks losing those correspondent relationships entirely. As the Decta analysis of crypto neobanks explains, this makes the rejection structural rather than case-by-case. The decision is not about a specific business; it is about the bank's own infrastructure dependencies.

The operational cost of being de-banked

What happens when businesses get rejected from creating a business bank account?:

- Cash flow breaks down. Receiving payments from customers or investors requires workarounds: personal accounts, intermediary wallets, or offshore arrangements that introduce friction and audit complexity.

- Investor credibility suffers. Institutional due diligence requires clean, auditable records. A company running expenses through a multi-sig wallet and a personal account cannot produce them.

- Compliance exposure accumulates. Routing business funds through personal accounts creates AML risk that typically surfaces at the worst possible moment, such as a licensing application or regulatory review.

For organizations seeking an alternative business bank account, such as crypto companies, the challenge is not just finding a willing provider. But also finding one built for the operational realities of a digital-asset business.

Understanding the License Behind the Platform

Not all crypto-friendly business accounts operate under the same regulatory framework. The licensing structure behind a provider shapes what services it can offer, how client funds are protected, and what oversight applies. Providers generally fall into three tiers, each with a different regulatory foundation.

Licensed Banks and Deposit-Taking Institutions

Banks sit at the most heavily regulated end of the spectrum. They hold full banking licenses, are subject to strict prudential requirements including capital adequacy, liquidity, and ongoing supervisory reporting, and handle fiat currency. In most jurisdictions, bank clients have access to government-backed deposit insurance. If the bank fails, eligible depositors receive an automatic payout up to a defined limit without going through an administration process.

The insurance scheme and coverage limit vary by jurisdiction. In the United States, the Federal Deposit Insurance Corporation (FDIC) insures deposits up to $250,000 per depositor per insured bank, per ownership category. In Hong Kong, the Hong Kong Deposit Protection Board (HKDPB) covers deposits up to HK$800,000 per depositor per bank, following an enhancement that came into effect in October 2024. Other jurisdictions operate their own schemes with different limits and eligibility rules.

When evaluating a provider in this tier, confirm which deposit protection scheme applies, what the coverage limit is, and whether your business qualifies as an eligible depositor. Some schemes exclude corporate depositors or apply different limits to business accounts.

Fewer crypto-friendly platforms hold full banking licenses because the capital requirements and regulatory overhead are substantially higher. In late 2025 and early 2026, a wave of crypto-native firms applied for or received conditional OCC national trust bank charter approvals in the United States, including Circle, Ripple, BitGo, and Paxos. For businesses holding significant treasury balances, a provider in this tier may offer more robust fund protection, but the level of protection depends on the jurisdiction and scheme in question.

Licensed Non-Bank Financial Institutions

Providers in this tier hold payment institution or electronic money licenses. They can issue electronic money and provide payment services but cannot take deposits in the legal sense or lend client funds.

The specific license name varies by jurisdiction. The EU uses the Electronic Money Institution (EMI) framework, complemented by the revised Payment Services Directive (PSD2) for payment service regulation. Singapore issues a Major Payment Institution (MPI) license under the Payment Services Act. Hong Kong issues a Stored Value Facility (SVF) license under the Payment Systems and Stored Value Facilities Ordinance. The United States has no direct federal equivalent, with money transmitter licenses varying by state.

The EMI minimum initial capital sits at €350,000, compared to several million euros typically required for a full banking license.

Despite the different names, the core protection model across most of these frameworks follows a safeguarding approach rather than a deposit guarantee scheme. Client funds are held in segregated accounts at licensed credit institutions, separate from the provider's own funds, and reconciled regularly. As InnReg summarises, safeguarding protects funds structurally rather than through an insurance-style guarantee. If the provider fails, those segregated funds are excluded from the insolvency estate, but recovery goes through an administration process rather than an automatic payout.

When evaluating a provider in this tier, confirm which license applies, in which jurisdiction it was issued, how client funds are segregated, and whether those arrangements are externally audited.

Crypto-Native Platforms

Many crypto-native platforms initially operated without dedicated regulatory frameworks, often structuring under trust arrangements or general corporate licenses. These platforms combine fiat payment capability with native blockchain integration, connecting to digital asset treasuries, supporting stablecoin-funded spending, and providing multi-currency expense management from a single dashboard.

That regulatory gap is closing. Jurisdictions worldwide are introducing dedicated frameworks for digital asset activity. These include Virtual Asset Service Provider (VASP) and Virtual Asset Trading Platform (VATP) licensing regimes, virtual asset dealing and brokerage licenses, custodian regimes for the holding of virtual assets, and stablecoin-specific licensing. Providers in this category may now hold one or more of these licenses, partner with a licensed bank, or operate under a combination of arrangements.

When evaluating a crypto-native provider, confirm which entity holds the license, in which jurisdiction, and what client fund protection framework applies. The regulatory landscape for these platforms continues to evolve, and the level of protection can differ significantly between providers.

What to Look For In A Web3 Crypto-Friendly Business Account

Before a crypto-friendly platform, most Web3 teams juggle exchanges, personal accounts and credit cards, and wallets to approximate a financial stack. With the right platform, those fragmented workflows collapse into a single, controlled environment. Evaluate providers against these criteria before committing:

1. Web3 and Crypto-native compliance capability.

Confirm what type of licenses the provider holds. Does the provider understand Web3 compliance infrastructure? Such as crypto-specific compliance needs, i.e., transaction monitoring for on-chain and off-chain flows, how entities are set up and their structures.

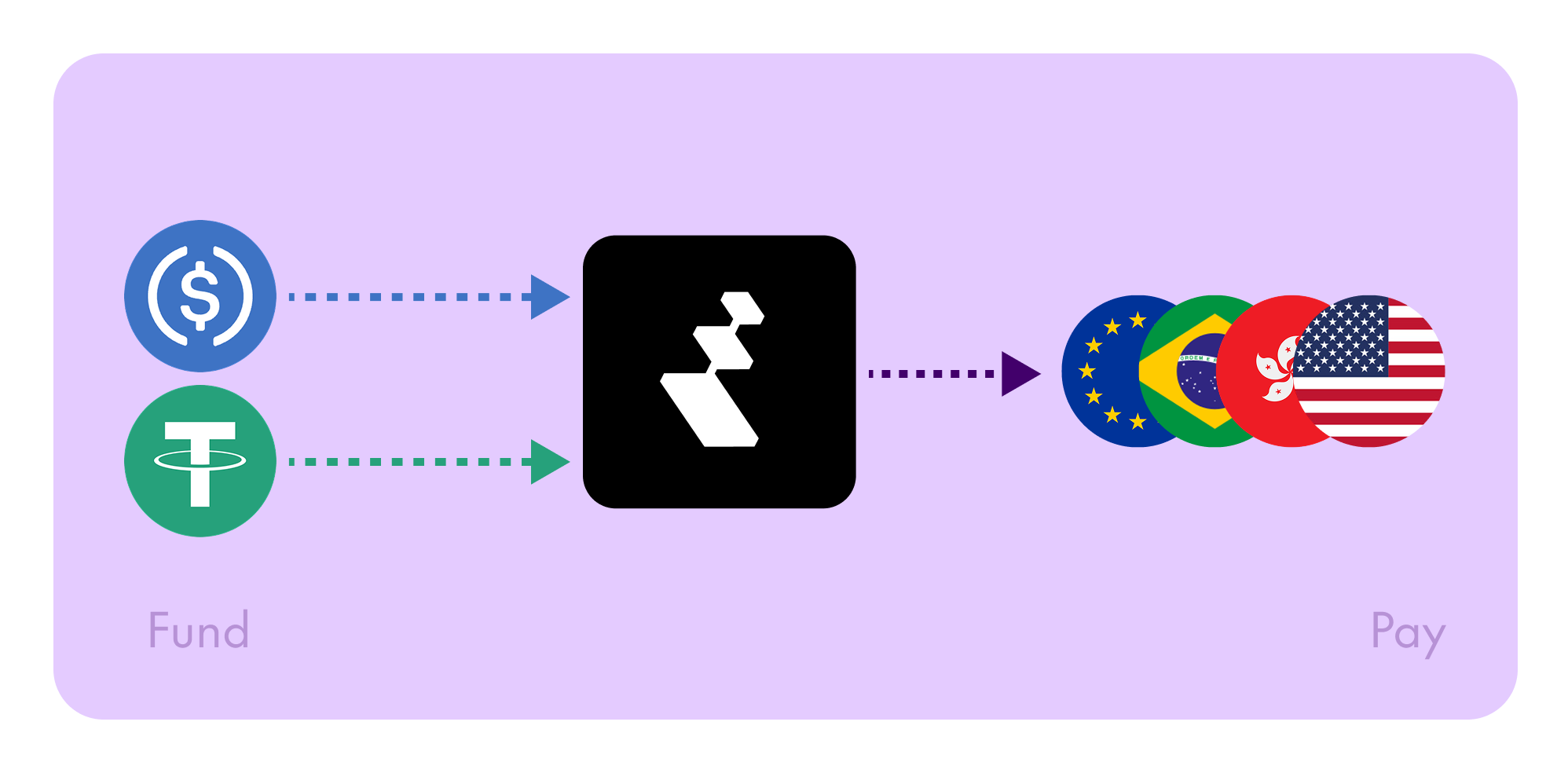

2. Stablecoin-native funding with fiat execution.

There is a meaningful difference between a platform that is okay working with crypto companies vs one with crypto-native infrastructure. The strongest providers let you fund in USDC or USDT and then spend, pay, and settle in local fiat currencies — without forcing a manual off-ramp at every step. This is the single biggest friction-reducer for a Web3 treasury: the ability to hold stablecoins as working capital while your cards, payroll, and vendor payments all execute in fiat seamlessly.

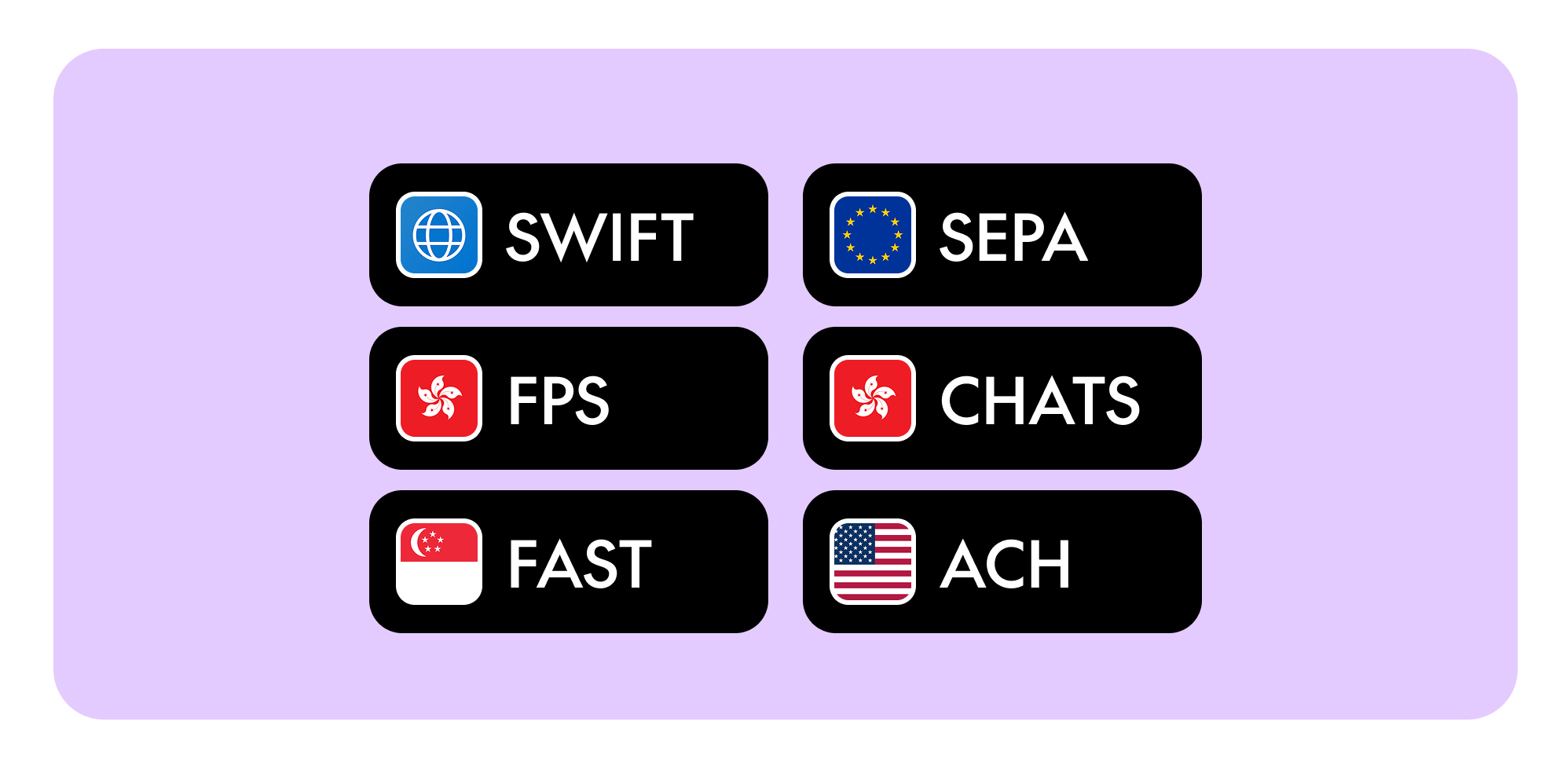

3. Currency coverage and speed of payments.

Verify which networks they access directly (SWIFT, SEPA, FPS, FAST, CHATS, ACH) versus through partners. A platform with multiple local rails can settle faster and cheaper than one relying solely on SWIFT. For a Web3 business paying contractors and vendors across regions, the ideal flow is simple: send from your stablecoin balance, and the recipient receives local currency in their bank account, same-day or next-day.

4. Expense controls and team governance.

A shared account with no access hierarchy creates operational risk the moment your team grows beyond the founders. Require role-based permissions, customizable approval workflows, individual card limits, and a unified dashboard where finance leads can monitor spend in real time. These controls should be built in, not bolted on through third-party expense software.

5. Onboarding and KYB/KYC speed.

Look for self-serve onboarding and a compliance team experienced with blockchain-sourced funds, with a clear verification flow. This reduces back-and-forth and prevents repeated submissions when the same business applies again.

What to Prepare: Documentation

Onboarding a crypto-friendly business account involves AML and KYB obligations. As a general industry practice across regulated payment institutions — including those operating under frameworks like the FATF Recommendations on Customer Due Diligence, which includes EU's Anti-Money Laundering Directives, and equivalent standards enforced by regulators such as MAS in Singapore and the FCA in the UK — most providers require the following when opening a business account:

- Certificate of incorporation and articles of association

- Corporate structure chart with all beneficial owners (UBOs) and ownership percentages — UBO thresholds typically start at 25% ownership, though some providers apply a lower threshold of 10%

- Government-issued identity documents for all authorized signatories, directors and UBOs above the applicable threshold

- Business model description: what the company does, how it earns revenue, and what types of transactions will flow through the account

- Source of funds documentation, including on-chain treasury origins for Web3 businesses

- Expected transaction profile: approximate monthly volumes, average transaction sizes, and key counterparties

Is It Truly Crypto-Friendly?

Many providers that describe themselves as "crypto-friendly" are primarily fiat-first financial platforms that are comfortable onboarding crypto businesses. They may allow SEPA transfers to and from crypto platforms and offer faster onboarding than a traditional bank. Meaningful, but not the same as platforms built for Web3 operations.

Often, these "crypto-friendly" business accounts typically support things like fiat accounts, local transfers, cards, and cross-border payouts to exchanges. In practice, it often assumes your business will convert digital assets to fiat first, then run operations in fiat. The conversion step remains a separate, manual process that the business must manage on its own.

A true crypto-friendly business account is crypto-native; designed around the reality that many Web3 teams hold treasury on-chain and need to run day-to-day operations across both crypto and fiat. It is built to support crypto and fiat workflows in one operating layer, rather than treating crypto as an external funding source that needs to be off-ramped before it becomes usable.

The gap becomes clear at specific operational requirements:

- Seamless treasury-to-spending. In a pseudo crypto-friendly setup, a team that holds treasury in digital assets like stablecoins must move funds to an exchange, convert to fiat, transfer to a bank account, and then spend on the business account. Each step introduces delays, fees, and reconciliation overhead. A true crypto-friendly business account removes those intermediate steps by allowing teams to spend from stablecoin balances, with the account handling expense execution seamlessly, whether for a corporate card transaction or a cross-border vendor payment.

- Visibility. A pseudo crypto-friendly account provides visibility into fiat transactions. Stablecoin inflows may appear as line items, but the platform has no native awareness of what those funds represent or how they fit into the broader treasury picture. A crypto-native platform treats stablecoin and fiat balances as part of the same financial view, with real-time tracking across both.

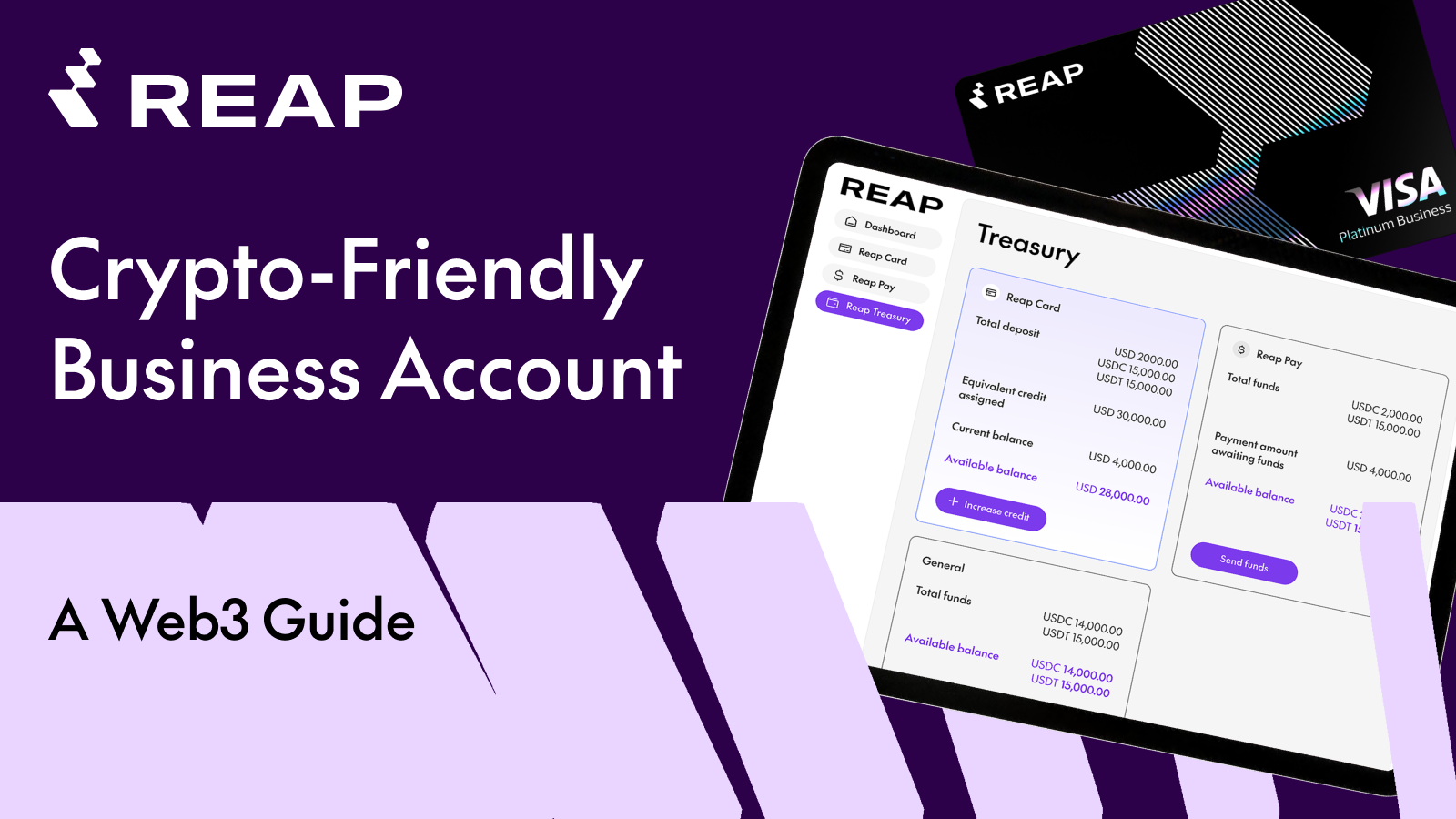

A True Crypto-Friendly Business Bank Account: Reap

Reap is an alternative to business bank accounts for crypto companies, acting as a layer for day-to-day operations by bringing cards, payments, and spend controls into one place.

Reap Direct is a self-serve financial platform designed for crypto-native and Web3 businesses.

Teams can fund using digital currencies (USDC/T) from supported blockchain networks, so crypto-native businesses can use digital-asset treasury funds to power fiat-denominated business spending through Reap Cards issued.

Reap's business account supports local and cross-border payments in major currencies across payment rails including SWIFT, SEPA, FPS, CHATS, and FAST.

It is designed to scale from small teams to more complex, multi-entity operations with global payment needs. Note that Reap is a licensed financial institution, not a bank.

In sum

Banking access is operational infrastructure for Web3 companies, as foundational as the protocols a company builds on. A crypto-friendly business account exists because the legacy banking system was not built for blockchain-native business models, and because most generic fintech accounts do not fully address the operational requirements of Web3 either.

Understanding what a genuine crypto-friendly platform does, how its licensing structure protects funds, what structural risks operate above the platform level, and how to combine it with traditional banking where that adds value gives a company the operational speed, compliance resilience, and financial credibility it needs to scale.

Disclaimer

The information provided in this material is for general informational purposes only and does not constitute legal, financial, tax, or business advice. It should not be interpreted as a recommendation, offer, solicitation, or inducement to engage with Reap's products or services. Any use of Reap's services is at the user's sole risk and discretion.

Reap makes no representation or warranty, express or implied, regarding the accuracy, completeness, or reliability of the information provided. Services are governed exclusively by Reap's applicable legal agreements. Service availability, features, and eligibility may vary by jurisdiction and are subject to regulatory, card network, and operational limitations.

All trademarks, logos, and brand names are the property of Reap and/or their respective owners. References to third-party platforms or services are for descriptive purposes only and do not imply endorsement, partnership, or affiliation.

Reap's services and information are provided on an "as is" and "as available" basis, without warranties of any kind. Reap shall not be liable for any loss or damage arising from the use of, or reliance on, this information or its services.